The High Cost of Cash: Why cash usage costs our economy R30 billion a year

August 1, 2025

Return to Blog ListAugust 1, 2025

Return to Blog List

South Africa’s payments landscape has evolved rapidly over the last decade. Today, consumers and businesses have access to a growing range of digital payment options, from debit and credit cards and mobile wallets to Pay by bank and QR code-based solutions. Yet, despite growing adoption of digital payments, cash remains the dominant payment method in South Africa, particularly in informal and rural areas, according to the South African Reserve Bank’s 2023 Payments Study.

This reliance on cash carries a significant economic burden. According to the Payments Association of South Africa’s (PASA) integrated report, released in June 2025, cash use costs the South African economy approximately R30 billion annually to facilitate and secure its circulation. So why does cash still reign supreme, and what can be done to shift towards more efficient, inclusive digital payment systems?

Cash may appear convenient, but its hidden costs are substantial and widespread. Before it reaches consumers, cash must be printed, stored, insured, transported, and distributed. All of this comes at a price:

All of these factors contribute to the R30 billion annual burden, affecting not only financial institutions and businesses but the broader economy. Even if consumers don’t directly see the cost, they’re paying for it in the form of bank fees, inflated retail prices, and reduced efficiency in the financial system.

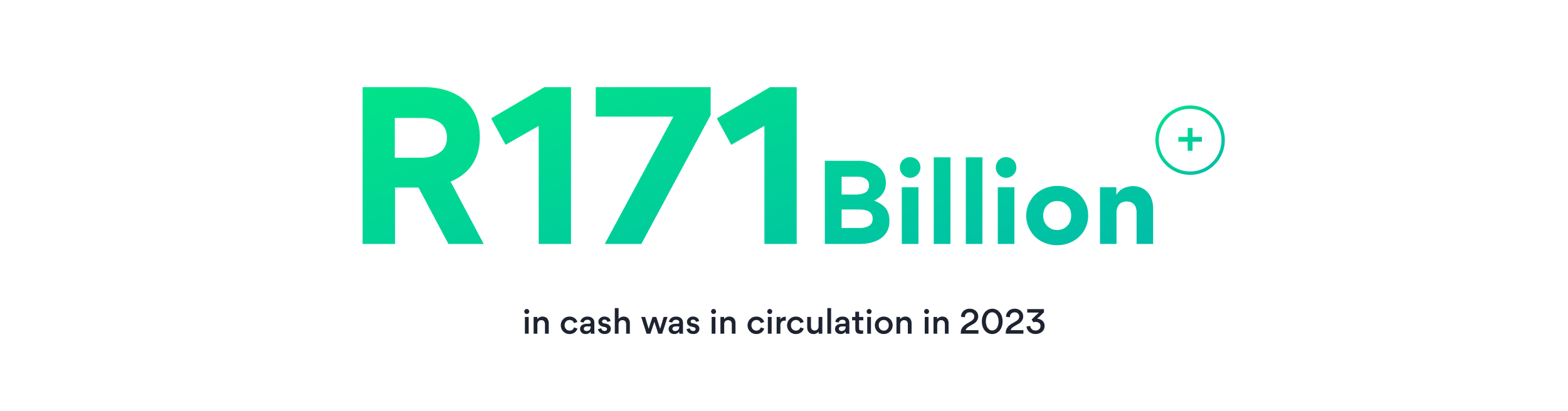

Despite significant innovation in the digital payments space, South Africa remains a cash-heavy society. According to the South African Reserve Bank, over R171 billion in cash was in circulation in 2023, a figure that has remained relatively consistent since 2009.

Several key challenges contribute to the slow shift away from cash:

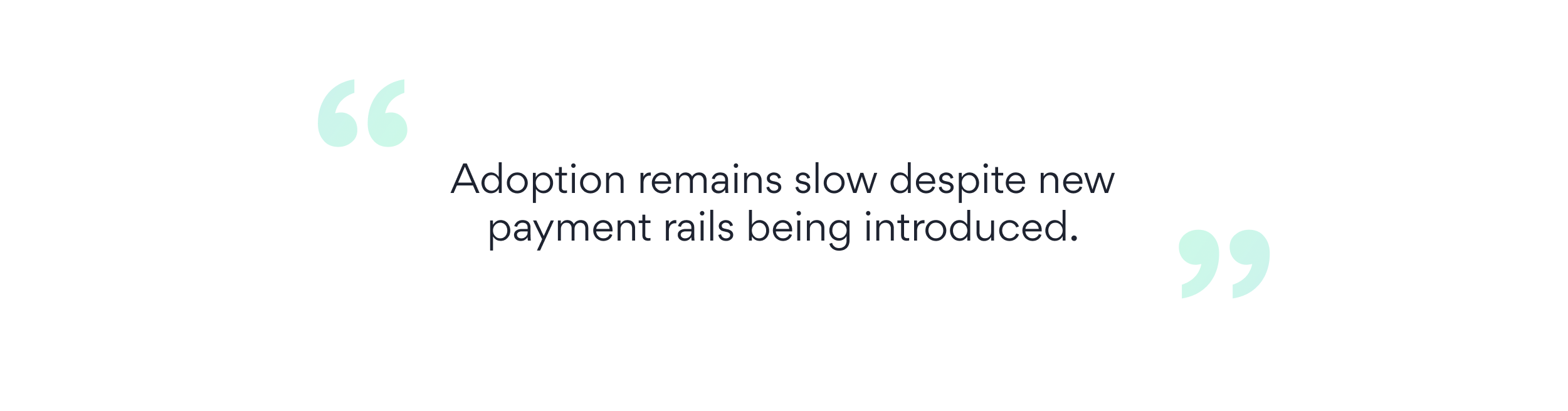

There have been notable strides towards a digital-first payment future, particularly with initiatives like PayShap, a real-time, low-cost payment system introduced to drive broader financial inclusion.

PayShap allows consumers and businesses to send and receive payments instantly, even across banks, with the added benefit of QR payment support. Since its launch, adoption has been steadily growing, and its potential to support small merchants and underserved consumers is increasingly evident.

Yet, as Tim Masela, Head of the National Payments System at the SARB, recently noted: “Adoption remains slow despite new payment rails being introduced.”

That’s because while infrastructure is improving, South Africa faces an inclusion and education challenge. Simply put, many South Africans are not yet in a position to adopt digital payments due to affordability constraints, infrastructure gaps, and a lack of awareness or trust.

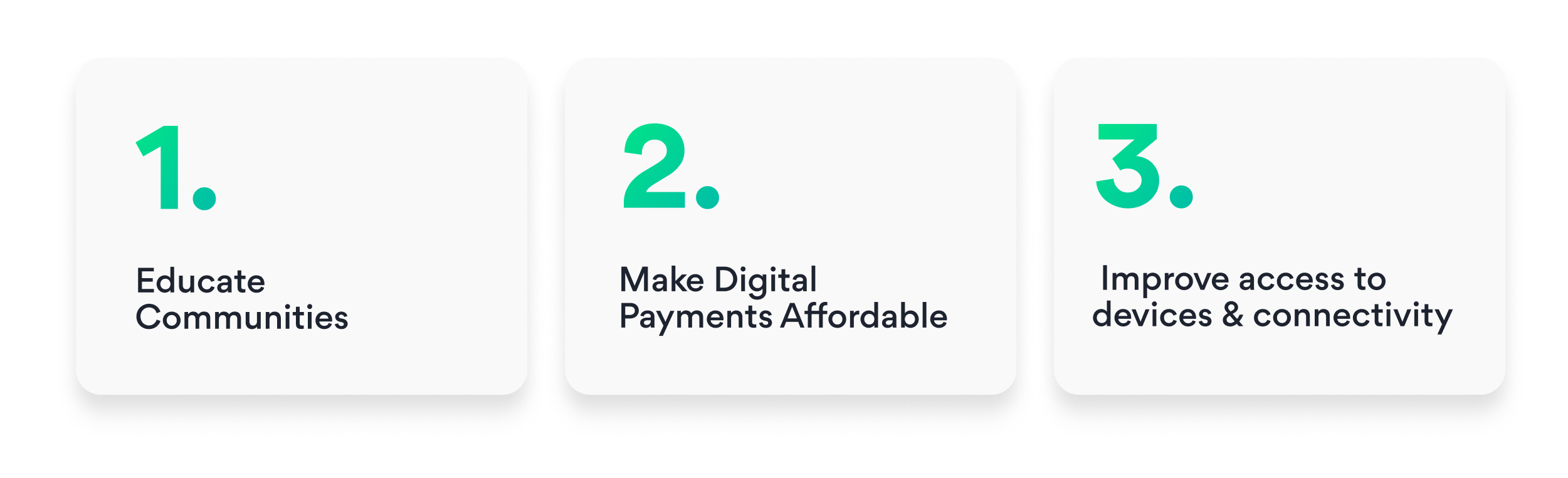

Solving South Africa’s cash problem won’t happen overnight, and it won’t happen without collective action across public and private sectors. Several interventions can help accelerate adoption:

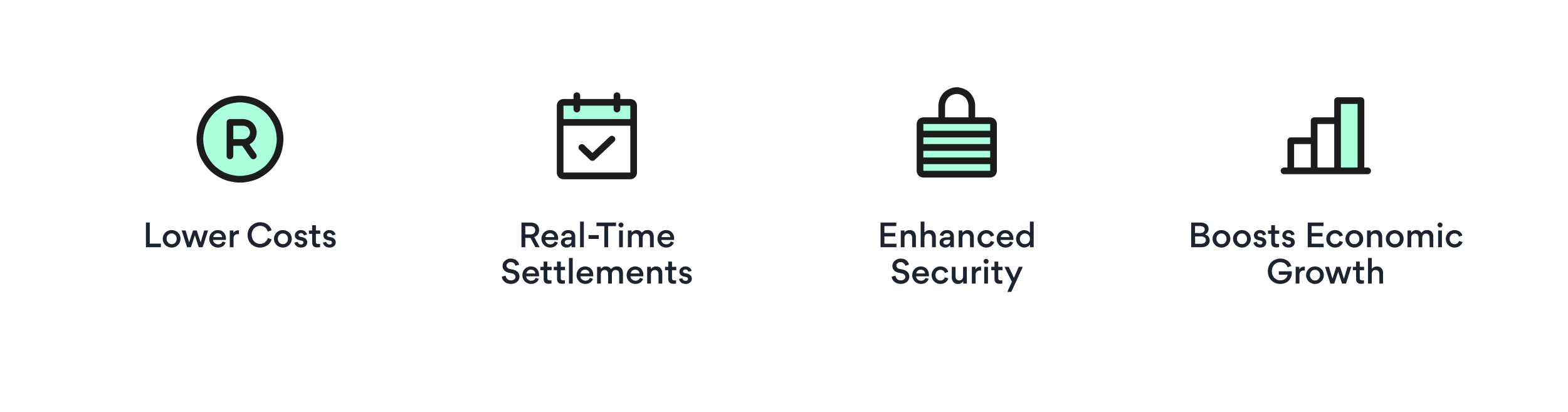

Accelerating the shift to digital payments has wide-reaching benefits:

The transition to a more digitally-enabled economy is not just a matter of convenience, it's an economic imperative. While South Africa has the infrastructure and innovation to lead in digital payments, adoption remains too slow to reverse the massive cost burden of cash.

By prioritising financial inclusion, lowering transaction costs, and bridging the digital divide, we can build a payment ecosystem that works for everyone, and unlock real growth for businesses, consumers, and the broader economy.